April 2018

The US Court of Appeals for the Federal Circuit’s recent decision in Exmark Manufacturing Company v. Briggs & Stratton Power Products Group, LLC (January 12, 2018) validates that there is no clear-cut method to value a patented invention’s contribution to a larger, multicomponent product (aka apportionment). Specifically, the Federal Circuit stated that “…apportionment can be addressed in a variety of ways…[so] long as [the patent owner] adequately and reliably apportions between the improved and conventional features” of the accused product. Along with providing this leniency, the Federal Circuit provided some (perhaps obvious) guidance to performing a “thorough and reliable analysis to apportion the royalty rate”: perform a “proper analysis of the Georgia-Pacific factors….the standard Georgia-Pacific reasonable royalty analysis takes account of the importance of the inventive contribution in determining the royalty rate that would have emerged from the hypothetical negotiation”. This guidance does not minimize the flexibility offered by the Federal Circuit in determining a reasonable royalty. After some case background, this article provides some examples of apportionment methods.

Case Background

Exmark Manufacturing Company (“Exmark”) sued Briggs & Stratton Power Products Group, LLC (“Briggs”) for infringing on claim 1 of its patent (U.S. Patent No. 5,987,863 (“’863”)). In short, the ‘863 patent relates to, inter alia, a lawn mower having improved flow control baffles (a metal structure under the mower deck) that direct air flow and grass clippings toward a side discharge opening more efficiently, resulting in improved quality of the mowing operation. Although the ‘863 patent contained other claims that relate to a complete lawn mower, both parties agreed that damages be apportioned between the improved baffles (the patented improvement) and the mower’s conventional components. In other words, the parties agreed that the royalty should apportion the value of the invention from the value of the lawn mower as a whole.

However, the parties disagreed as to the apportion valuation method. Specifically, they disagreed on the proper royalty base: whether the royalty base includes only the patented improved baffles or the entire lawn mower. Establishing the proper royalty base involves the Entire Market Value Rule, which is generally defined as follows: If the patented feature drives the demand for the product, then it may be appropriate to consider some or all of the profits from the sale of the product in determining the appropriate royalty rate. However, if the patented feature does not drive the demand for the product containing the patented feature(s), one must apportion the profit before selecting the reasonable royalty rate.

Exmark used the entire lawn mower sales price as the royalty base and adjusted the royalty to apportion value attributable to the patented improved baffles. Briggs argued that the Entire Market Value Rule required using something less than the entire lawn mower sales as the royalty base. The district court rejected Briggs’ argument, stating that, “The claimed benefits of the invention – improved cutting performance, a reduction of blowout, a more uniform discharge, and a faster cut with less engine demand – all go to the heart of the purpose and function of the accused product.”

On appeal, Defendants argued, inter alia, that the district court wrongly permitted Exmark to use the sales price of the entire lawn mower as the royalty base rather than the sales price of the patented improved baffles. The Federal Circuit disagreed as follows:

“We have held that apportionment can be addressed in a variety of ways, including ‘by careful selection of the royalty base to reflect the value added by the patented feature [or] . . . by adjustment of the royalty rate so as to discount the value of a product’s non-patented features; or by a combination thereof.’ Ericsson, 773 F.3d at 1226. So long as Exmark adequately and reliably apportions between the improved and conventional features of the accused mower, using the accused mower as a royalty base and apportioning through the royalty rate is an acceptable methodology. Id. (citing Garretson, 111 U.S. at 121). ‘The essential requirement is that the ultimate reasonable royalty award must be based on the incremental value that the patented invention adds to the end product.’ Id.”

…We hold that such apportionment can be done in this case through a thorough and reliable analysis to apportion the royalty rate. We have recognized that one possible way to do this is through a proper analysis of the Georgia-Pacific factors. See Georgia-Pacific Corp. v. U.S. Plywood Corp., 318 F. Supp. 1116 (S.D.N.Y. 1970). As we have explained, ‘the standard Georgia-Pacific reasonable royalty analysis takes account of the importance of the inventive contribution in determining the royalty rate that would have emerged from the hypothetical negotiation.’ AstraZeneca, 782 F.3d at 1338.

…Exmark’s use of the accused lawn mower sales as the royalty base is consistent with the realities of a hypothetical negotiation and accurately reflects the real-world bargaining that occurs, particularly in licensing. As we stated in Lucent Technologies, Inc. v. Gateway, Inc., ‘[t]he hypothetical negotiation tries, as best as possible, to recreate the ex ante licensing negotiation scenario and to describe the resulting agreement.’ 580 F.3d 1301, 1325 (Fed. Cir. 2009). ‘[S]ophisticated parties routinely enter into license agreements that base the value of the patented inventions as a percentage of the commercial products’ sales price,’ and thus ‘[t]here is nothing inherently wrong with using the market value of the entire product, especially when there is no established market value for the infringing component or feature, so long as the multiplier accounts for the proportion of the base represented by the infringing component or feature.’ Id. at 1339.”.

Examples of Apportionment Methods

Generally, the Federal Circuit allowed the use of the Entire Market Value Rule when supported by the correct facts, but insists that the rule not be misapplied, as is discussed in this related article regarding LaserDynamics v. Quanta Computer, Case No. 11-1440 (Aug. 30, 2012). The Rule may sometimes be justified because it is difficult to know the component’s value to which a percentage royalty is applied. Considering the Georgia Pacific factors in performing a reasonable royalty analyses, Georgia Pacific factor #13 states:

“The portion of the realizable profit that should be credited to the invention as distinguished from non-patented elements, the manufacturing process, business risks, or significant features or improvement added by the infringer”.

This apportionment can be one of the more challenging factors in a reasonable royalty analysis. Some circumstances allow a more simple analysis that defines the next best alternative(s) that account for the value of the non-patented elements. Other cases may require more work. Sometimes using multiple apportionment methodologies that arrive at a similar conclusions can strengthen the apportionment value conclusion. Examples of methods to apportion the profit attributable to the patented feature(s) are provided below. Note that these methods may not be appropriate/applicable in all cases. Additionally, each one of these methods by itself may not be sufficient for an apportionment value conclusion:

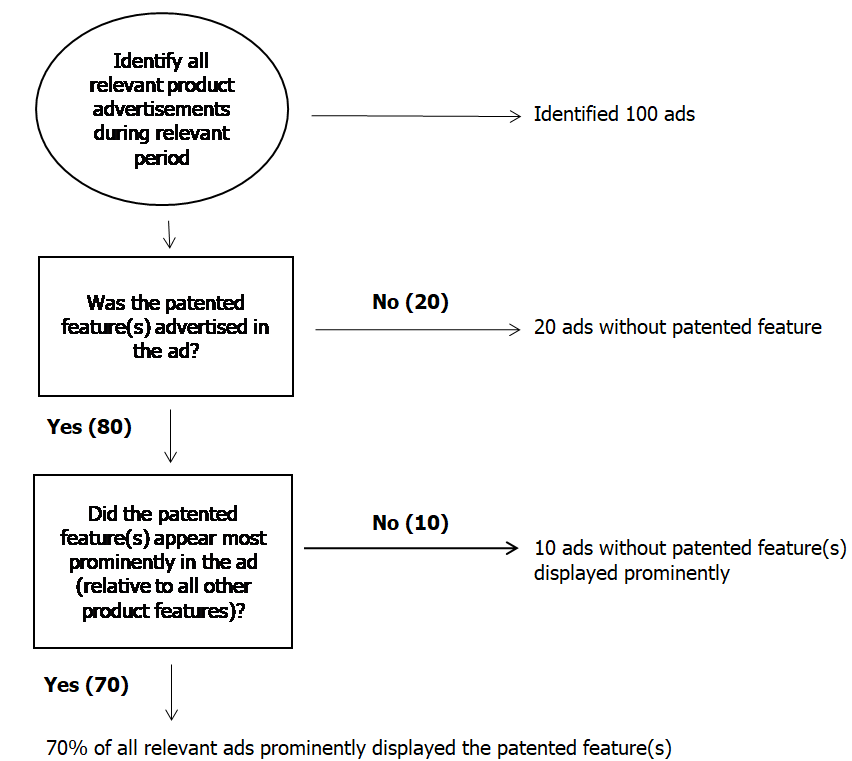

- Advertisements – If the product that contains the patented feature(s) has been advertised during the relevant period, consider the product advertisements. Advertising (or lack thereof) may indicate a measure of value of the patented feature(s). The following flow chart provides a simplified example:

One may infer from the above simplified example that much of the product’s value relates to the patented features.

- Sales comparison – Compare the volume of product sales that contain the patented feature relative to product sales of otherwise similar product(s) without patented feature(s). A simple example: if two products (one with and one without the patented feature) have similar sales volumes during similar time periods to similar consumers and geographic regions, one may infer that the patented feature may not add much incremental value.

- Required rate of return – Disaggregate the resources used in making the product with the patented feature and calculate the required rate of return on each resource so that the company remains viable. Notably, this method is likely one of the less practicable due to, inter alia, a lack of data available for the calculation.

In matters where apportionment needs to be addressed, it is helpful to get a damages expert involved early in the process so that you have a reasonable assessment of the value of the claim. Fulcrum Inquiry regularly assesses damages in intellectual property litigation as a damages expert witness.